How Conventional Planning Fails to Provide Sound Financial Advice

Jay Abolofia, PhD, CFP® is a fee-only, fiduciary & independent financial planner in Waltham, MA serving clients in Greater Boston, New England & throughout the country. Lyon Financial Planning provides advice-only comprehensive financial planning for a flat fee to help clients in all financial situations.

In financial planning, sometimes getting it right is more about not getting it wrong. This makes rules of thumb dangerous to your financial well-being. Nonetheless, that is exactly what conventional planning uses to generate its recommendations. Fortunately, economics-based planning offers a sound alternative.

In what follows I describe how and why conventional planning fails to provide sound financial advice, and introduce an economics-based alternative that relies on facts and common sense. In doing so, I focus on three of the most important financial questions you face:

How much can you afford to spend?

How much insurance is required?

How much investment risk can you afford to take?

Why Conventional Financial Planning Fails

Rather than figure out how much you can actually afford to spend, conventional planning asks you to guess. Yes, that’s right! Conventional planning asks you to guess how much you will spend in retirement, even if retirement is over thirty years away.

To formulate its guess, conventional planning assumes that your household’s retirement spending will be 70-85% of your pre-retirement income. This so-called income-replacement ratio is based on historical averages across US households. In other words, it has nothing to do with you.

Every core recommendation you receive from conventional planning stems from this one guess. Larry Kotlikoff, professor of economics at Boston University, points out that this is a serious problem. First, no one can accurately guess how much they will spend in retirement. It’s immensely complicated. Second, even if you could, it would be near impossible to translate that into accurate spending, saving, insurance and investment recommendations.

How Conventional Financial Planning Fails

When you meet with your financial planner you are trusting them to provide sound financial advice—recommendations that help you get to where you want to go. Unfortunately, by basing its recommendations on rules of thumb, the conventional approach inadvertently delivers advice that is wholly inaccurate.

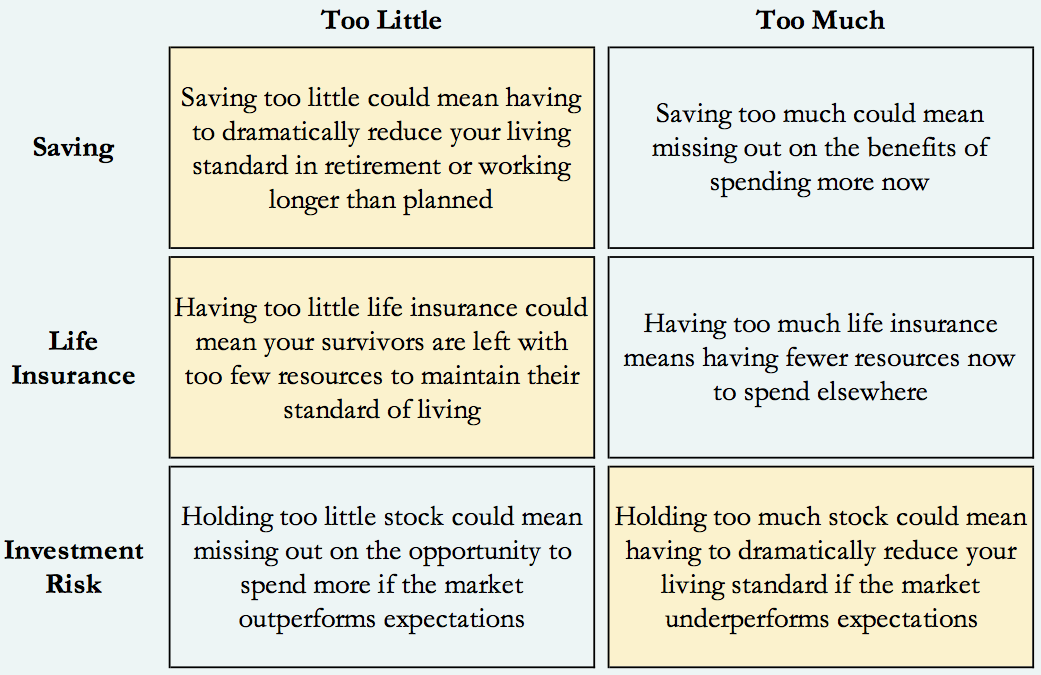

Getting it wrong, when it comes to certain financial decisions, might not be such a big deal. For example, spending too much on a car or even a home renovation may be disruptive, whereas failing to save enough for retirement, not having adequate life insurance or holding too much stock in your investments may be devastating. Consider the impacts of getting one of these decisions wrong. If you are reluctant to take risks, like most people, you’ll be especially concerned with the highlighted outcomes.

Economics-Based Financial Planning

Fortunately, there’s an alternative to conventional planning—an economics-based approach that relies not on rules of thumb, but on facts and common sense. Economics-based planning removes the guesswork by actually solving for how much you can afford to spend now and in retirement. This generates accurate recommendations for spending and saving, life insurance and investment risk.

To do so, economics-based planning employs the common sense idea that people prefer to maintain a smooth standard of living throughout their lives. In essence, no one wants to splurge today and starve tomorrow, or vice versa. Combining this idea with the fact that you can’t spend more over your lifetime than you have in resources, allows you to accurately estimate how much spending is affordable and saving is required throughout your life.

Don’t Leave Your Financial Future to Guesswork

The objective of financial planning is to make well-informed decisions that best optimize your current and future financial situation. Making a wrong decision, especially when doing so based on professional advice, can be a tough pill to swallow. Fortunately, there’s an alternative to conventional planning that doesn’t rely on guesswork.

By combining facts and common sense, economics-based planning provides accurate recommendations for the most important financial decisions you face. Knowing how much you can afford to spend means you’ll be saving the right amount for your retirement and other big goals. Having the right amount of life insurance means your spouse and children will be protected if something happens to you. Knowing how much stock you can afford to hold in your investments provides peace of mind and long-term financial security through the ups and downs of the market.