How to Create an Effective Estate Plan

Jay Abolofia, PhD, CFP® is a fee-only, fiduciary & independent financial planner in Waltham, MA serving clients in Greater Boston, New England & throughout the country. Lyon Financial Planning provides advice-only comprehensive financial planning for a flat fee to help clients in all financial situations.

An estate plan is used to organize your personal and financial affairs in order to prepare for the future, including the unexpected. Having a sound estate plan is both a gift to your future self and your loved ones. This process is important for everyone, no matter the size of your estate. Without one, the laws of your State and the courts can control the process.

Will-Based vs Trust-Based Estate Plans

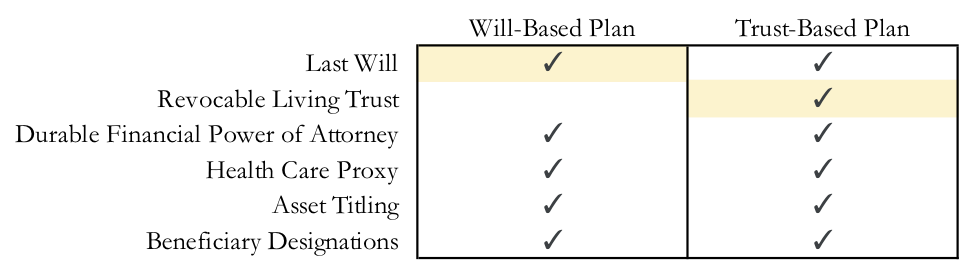

Your estate plan includes various documents, as well as asset ownership and beneficiary designations. Each component serves a different role, either during life or after death. If the plan involves a living trust, you have a trust-based estate plan. If not, you have a will-based estate plan. Below is a list of the various components of your plan, with the key element highlighted for each type.

A will-based estate plan revolves around your last will—a document that outlines who will distribute and inherit your property, and who will take guardianship of your minor children upon your death. Without a valid last will, the laws of your State and the courts will make decisions on your behalf. Depending on your wishes, your State’s plan may differ dramatically from your own. As part of your last will, you may choose to include a testamentary trust that goes into effect only after you die. Such a trust can be used to distribute your property to children or disabled relatives in accordance with your wishes.

A trust-based estate plan centers around your revocable living trust—a legal entity created to manage your property during life and distribute it after death. Like a will, your living trust can provide for the distribution of certain assets upon your death. Unlike a will, it allows you to authorize a successor trustee to manage your trust assets should you become incapable.

The primary advantage of a trust-based plan, over a will-based plan, is that it enables you to fully avoid probate—the court supervised process of settling your estate after you die. (Note that avoiding probate is different than avoiding estate taxes!) The probate process involves time (several months to a year), fees (up to 5% of the value of your probate estate) and lacks privacy (wills become public record). Avoiding probate makes the most sense if you have significant non-retirement assets, like real estate and investment accounts.

In some cases, a trust-based plan can also make the process of handling incapacity more efficient. If you become incapacitated, the designated successor trustee of your living trust can immediately take over management of assets in your trust. This avoids relying solely on your durable financial power of attorney arrangement, as with will-based plans, or the court supervised appointment of a conservator.

No matter the type of plan you have, designating a health care proxy is important. This document grants a person of your choosing the authority to make medical decisions on your behalf in the event that you are incapable. In addition, having a conversation with loved ones about your wishes for end-of-life care and creating a living will can be invaluable.

Implementing and Reviewing Your Estate Plan

Implementing your estate plan involves time and paperwork. Do-it-yourselfers may consider using an online resource like LegalZoom, while others may want to hire an estate-planning attorney. Either way, it’s sensible to have a local attorney review your documents before you print, sign and notarize them, and to provide specific advice on asset titling and beneficiary designations. Original documents may be kept in a fire proof safe in your home and digital copies may be shared with loved ones. Another important step is to draft a simple roadmap for your heirs that includes a summary of your assets and how the plan is designed to work. If you hire an attorney, ask them to help with this.

If you have a trust-based plan it is critical that you retitle your assets, that would otherwise go through probate, to the name of your living trust. In general, any asset that does not have a beneficiary designation will need to be owned by your trust (e.g., real estate, bank accounts and non-retirement investment accounts). Do not expect your attorney to do this for you! If you have a financial planner, ask them to help. Without completing this step, your assets will not avoid probate and your plan may not function properly.

It's good to review your plan every few years to make sure it still functions according to your wishes, especially if your financial or life situation has changed. Maintaining an up-to-date estate plan ensures that all your hard work will pay off, if and when it’s needed most.